Critical Minerals: The Hidden Bottleneck of Clean Energy

No Clean Energy Without Critical Minerals

Every solar panel, wind turbine, EV battery, and grid-scale storage system depends on a small set of critical minerals. The energy transition is often framed as a shift from fossil fuels to renewables — but it is equally a shift from oil dependency to mineral dependency.

The question is: who controls these minerals?

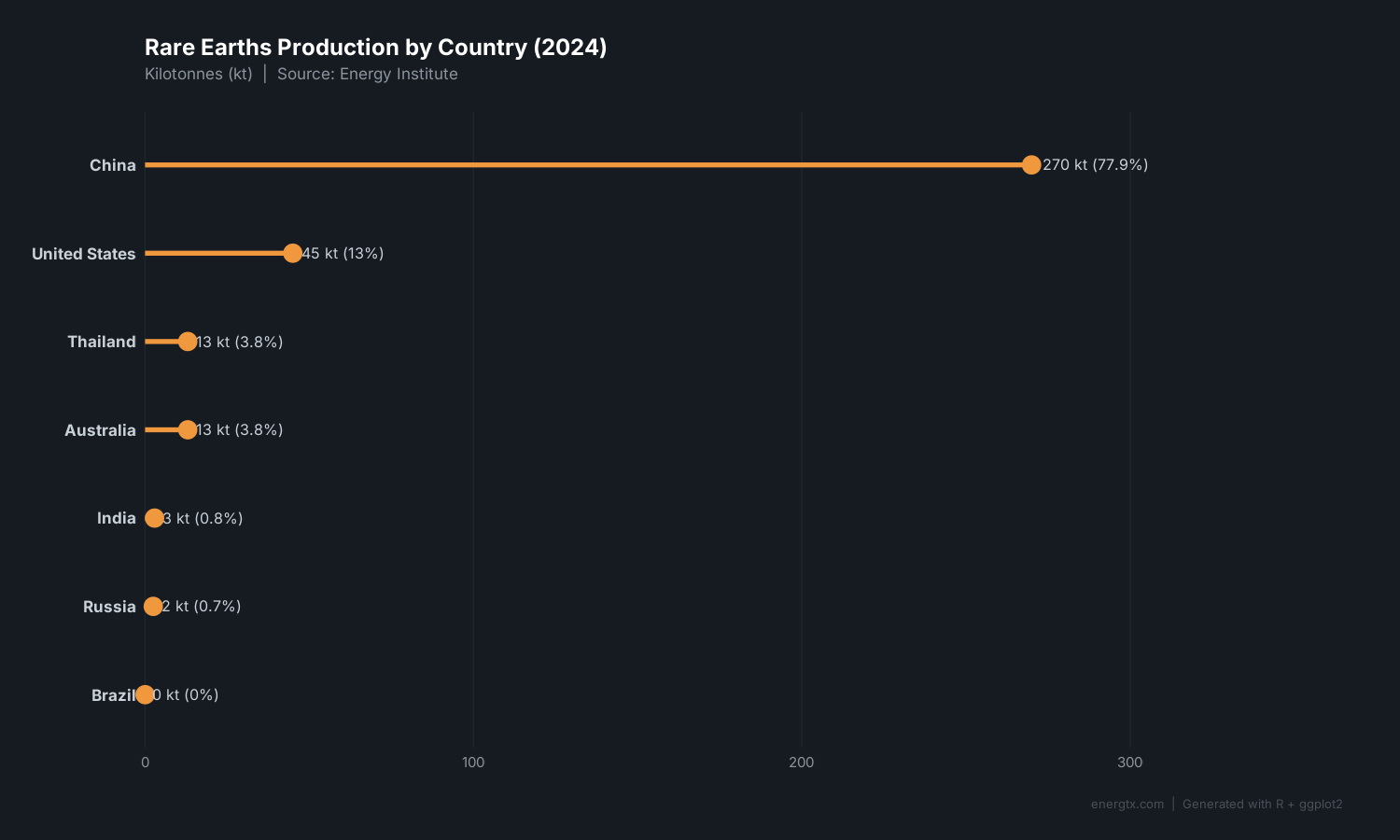

Rare Earths: China's Dominance

Rare earth elements are essential for permanent magnets used in wind turbines and EV motors. The production landscape is stark:

| Country | Production (kt) | Global Share | |---------|-----------------|-------------| | China | 270 | 77.9% | | United States | 45 | 13.0% | | Thailand | 13 | 3.8% | | Australia | 13 | 3.8% | | India | 3 | 0.8% |

China produces nearly 78% of the world's rare earths. This concentration creates significant supply chain vulnerability. Export restrictions, trade disputes, or domestic policy changes in a single country could disrupt global clean energy manufacturing.

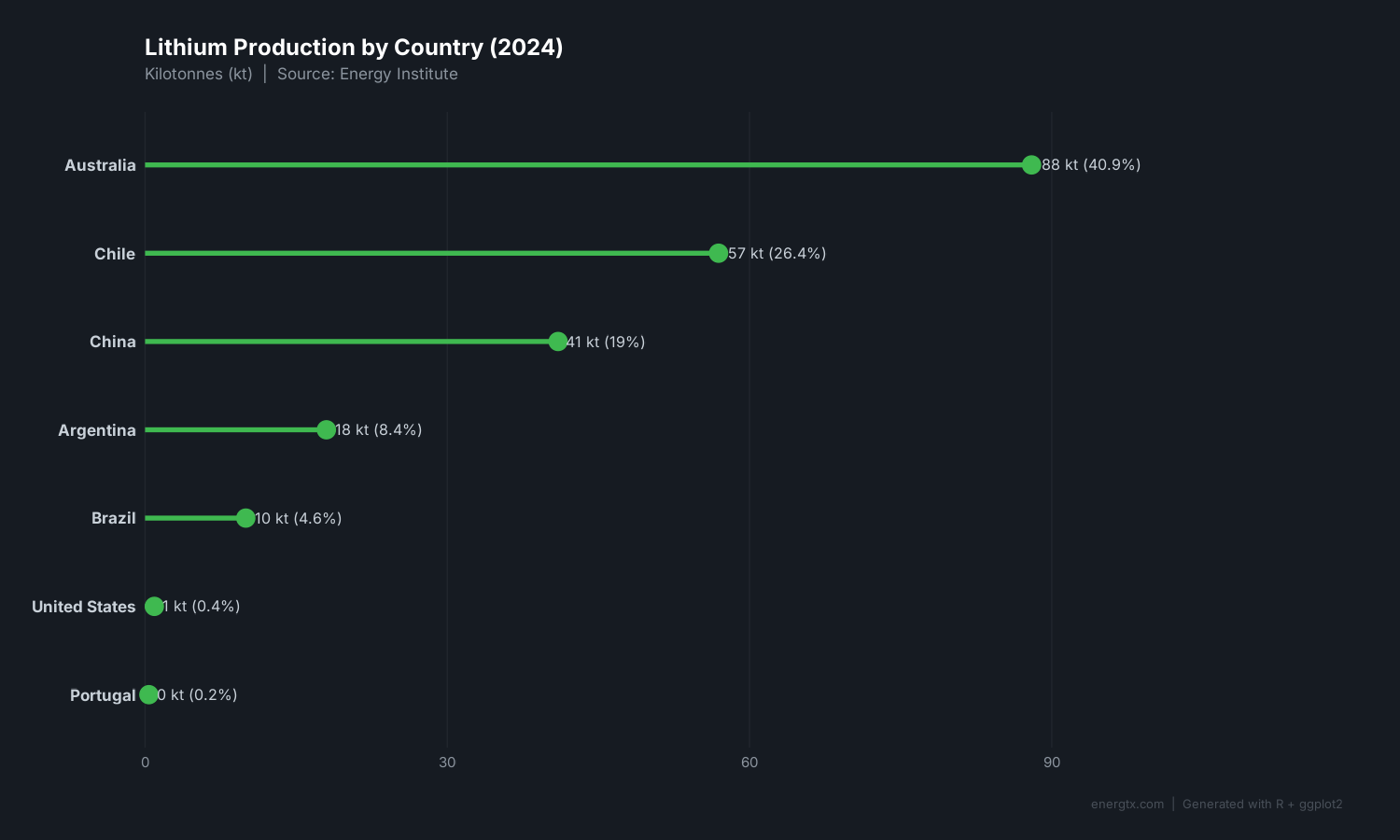

Lithium: The Battery Metal

Lithium is the backbone of modern battery technology. The supply picture is more diversified than rare earths, but still concentrated:

- Australia leads production with 88 kt, primarily from hard-rock spodumene mining

- Chile follows with 57 kt from brine evaporation in the Atacama Desert

- China produces 41 kt and is investing heavily in refining capacity

- Argentina and Brazil are scaling up as the "Lithium Triangle" expands

What This Means for the Energy Transition

Supply Chain Risk

The International Energy Agency projects that demand for lithium will grow 40x by 2040 under a net-zero scenario. Current production levels are insufficient to meet this demand without massive new mining investment.

Geopolitical Implications

Control of critical mineral supply chains is becoming a key element of energy security — analogous to oil supply in the 20th century. Countries are responding with industrial policies:

- The EU Critical Raw Materials Act aims to diversify supply

- The US Inflation Reduction Act incentivizes domestic mineral processing

- China continues to invest in mining assets across Africa and South America

The Recycling Imperative

As the first generation of EV batteries and wind turbines reaches end-of-life, urban mining (recycling minerals from spent products) will become increasingly important. Some estimates suggest recycled lithium could meet 10-15% of demand by 2035.

Explore the Data

Lithium, cobalt, and rare earths production data for all major producing countries is available on energtx.com. Compare production trends, explore country profiles, and download data in your preferred format.

The energy transition is not just about building solar panels and wind turbines — it is about securing the minerals that make them possible.

Methodology

Production data sourced from the Energy Institute Statistical Review of World Energy (2024 edition). Values in kilotonnes (kt). Visualizations generated with R and ggplot2.